China’s economy

Fears of a hard landing

China ran a massive trade deficit in February. What does it say about the economy?

Mar 17th 2012 | BEIJING | from the print edition

CHINA is routinely accused of exporting too much. Its foreign sales far exceed its foreign purchases, often by a wide margin. This chronic surplus angers many. This week President Barack Obama signed a bill that restores his administration’s power to impose tariffs on countries like China and Vietnam, when their goods are reckoned to be subsidised or dumped on American markets. The bill passed swiftly through both chambers of Congress. When it comes to rebuffing China’s exports, America’s fractious legislature is as harmonious as the Chinese one.

But this month brought two intriguing breaks to the routine. On March 13th three of China’s biggest trading partners—Japan, the European Union and America—complained that China was exporting too little, not too much. They brought a case at the World Trade Organisation alleging that China was unfairly restricting its exports of tungsten, molybdenum and 17 “rare earths”, obscure elements such as terbium and europium, used in the manufacture of many high-tech goods including fluorescent lights. China’s reaction was incandescent; it dismissed the case as “groundless”.

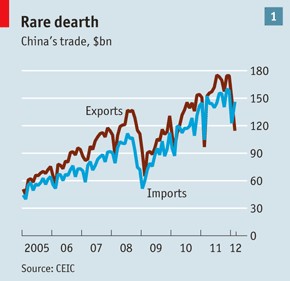

The other novelty arrived a few days earlier when China’s customs bureau reported something rarer than europium: a Chinese trade deficit. At $31.5 billion in February, the imbalance was bigger than any deficit on record—it was bigger even than many of China’s monthly surpluses.

In this section

· »Fears of a hard landing

China’s trade balance often dips around Chinese New Year, as export factories close for the festival. The holiday also arrived earlier this year than last, distorting the data. But even if the figures for January and February are added together, China ran a deficit of over $4 billion. Exports and imports typically rebound in sync as China gets back to work. This year, imports rebounded alone (see chart 1).

The deficit has fuelled one fear and one hope. The fear is that China’s economy will slow sharply, hobbled by declining exports to crisis-racked Europe and a rising bill for commodities like oil. The hope is that China is rebalancing, moving away from an economic model reliant on foreign demand. Neither the hope nor the fear is wholly justified by this month’s figures.

It is true that China’s weak exports are contributing to a slowdown in the broader economy. China’s industrial production grew by 11.4% in January and February, compared with the same two months in 2010, much slower than its normal pace of about 15%. But the prospects for global growth are brightening, suggesting that China’s exports have bottomed out. And the slowdown in China’s economy has been matched by a helpful fall in inflation. That gives China’s government some scope to stimulate demand.

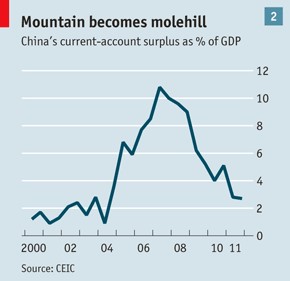

What about rebalancing? February’s trade deficit may be an anomaly but it highlights a broader trend: the swift decline in China’s external imbalance. China’s current-account surplus, a broad measure of the country’s external payments and receipts for goods and services, fell to 2.8% of GDP last year from a peak of over 10% of GDP before the financial crisis (see chart 2). In Hong Kong’s currency-derivatives market people no longer bet that the yuan will only strengthen. That suggests the yuan is close to its “equilibrium” level, said Wen Jiabao, China’s prime minister.

Unfortunately, China has rebalanced externally without rebalancing internally. Its current-account surplus has narrowed largely because of an increase in domestic investment, not consumption. Some economists therefore worry that China’s trade surpluses will soon reappear. An investment boom from 2001-04, for example, paved the way for the ballooning surplus of 2004-07, according to Jonathan Anderson, formerly of UBS. That investment poured into heavy industries, such as aluminium, machine tools, cement, chemicals and steel. This domestic supply displaced imports of the same products. And when a slowdown in China’s construction industry subsequently depressed domestic demand for these items, China sold abroad what it could no longer sell at home. Big surpluses were the result.

In the past three years, China has also enjoyed a terrific investment boom. And with the property market weakening, the construction industry is also liable to slow again. Is the stage therefore set for a repeat of the surpluses of 2004-07?

The difference now is the nature of China’s investment boom, which has concentrated on roads, railways and houses, not factories. In 2009, for example, loans for fixed investment increased dramatically. But only 10% were made to manufacturers, says Nicholas Lardy of the Peterson Institute. About 50% went to infrastructure projects. In his annual review of the government’s work this month, Mr Wen noted that China had shut down outdated factories capable of making as much as 150m tonnes of cement and 31.2m tonnes of iron.

Efforts to rationalise heavy industries and remove excess capacity should help prevent a repeat of the big external surpluses of yesteryear. That should, in turn, placate China’s irritable trading partners. But things might not be so simple. Take one particularly fragmented and dirty industry. At the government’s urging, one of its bigger firms has bought over a dozen others, eight of which were later shut down. That has reduced the industry’s capacity to flood the world with its products. The problem? These products are rare earths.

from the print edition | Finance and economics

· Recommended

· 19

附一篇在前一期的「金融與經濟」類的評論及下一篇「企業」類的對「中國製造」的擺脫廉價力的刻板印象的看法

China’s new growth targets

Year of the tortoise

China seeks (slightly) slower growth

Mar 10th 2012 | BEIJING | from the print edition

THE annual meeting of the National People’s Congress (NPC) draws almost 3,000 delegates to Beijing to listen to the Chinese government’s progress reports, rubber-stamp its proposals—and advance its goal of boosting consumption. At Silk Street Market, a Beijing institution, a digital banner welcomes the delegates to town and invites them to go shopping.

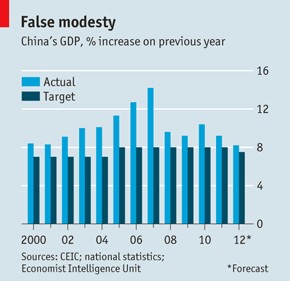

But if this year’s meeting lifted the fortunes of Silk Street stallholders, it dampened the animal spirits of others. They were perturbed by the opening speech, in which Wen Jiabao, China’s prime minister, set a growth target of just 7.5% for 2012. That is half a percentage point lower than the target set in the previous seven years. It is also below the 8% threshold deemed necessary to preserve social stability by some officials. His announcement was received badly by the region’s stockmarkets, especially in Australia, which is getting filthy rich selling its dirt (iron ore, coal, minerals) to China’s fast-expanding industries.

In this section

· »Year of the tortoise

If the government’s target were likely to be hit, the gloom would be easy to understand. But China routinely surpasses its targets, often by large margins (see chart). In fact, China’s recorded growth has fallen below 8% only twice in the past 20 years.

That was in 1998 and 1999, in the wake of the Asian financial crisis. That may also be when the notion took hold that China had to grow by at least 8% to generate enough jobs for the millions entering the labour force each year. China’s labour force is not, however, growing as quickly as it was. From 1991 to 2000, it swelled by 8.7m a year. This year it is projected to grow by less than 5.2m, which should mean China can get away with slower growth.

Unfortunately, China also does not create as many jobs as it did. As Nicholas Lardy of the Peterson Institute for International Economics has pointed out, employment outside agriculture grew faster from 1991 to 2001 than it did from 2003 to 2010, even though GDP growth was slightly brisker over the later period. This is because recent growth has been skewed towards manufacturing, not services, and towards capital-intensive manufacturing, not the labour-intensive kind. According to Mr Lardy, “balanced growth” of less than 8% would raise employment, wages and private consumption faster than unbalanced growth of much more than 8%.

By setting a lower growth target, the government may be indicating that it is willing to sacrifice some speed for better balance. That would be in keeping with the government’s longstanding rhetoric, if not its actions. Two years ago, for example, it released “36 guidelines” that were supposed to encourage private investment in parts of the economy, many of them services, traditionally dominated by state-owned enterprises. In this week’s speech, Mr Wen said he would adopt “specific operating rules” that might belatedly give those guidelines some bite.

A shift to less capital-intensive growth, if it were to happen, would be bad news for commodity exporters like Australia and good news for China’s neglected service industries, retailers included. In the meantime, Silk Street shopkeepers can be forgiven for caring more about the delegates’ patronage than their proposals.

from the print edition | Finance and economics

Manufacturing

The end of cheap China

What do soaring Chinese wages mean for global manufacturing?

Mar 10th 2012 | HONG KONG AND SHENZHEN | from the print edition

TRAVEL by ferry from Hong Kong to Shenzhen, in one of the regions that makes China the workshop of the world, and an enormousbillboard greets you: “Time is Money, Efficiency is Life”.

China is the world’s largest manufacturing power. Its output of televisions, smartphones, steel pipes and other things you can drop on your foot surpassed America’s in 2010. China now accounts for a fifth of global manufacturing. Its factories have made so much, so cheaply that they have curbed inflation in many of its trading partners. But the era of cheap China may be drawing to a close.

In this section

· »The end of cheap China

Costs are soaring, starting in the coastal provinces where factories have historically clustered (see map). Increases in land prices, environmental and safety regulations and taxes all play a part. The biggest factor, though, is labour.

On March 5th Standard Chartered, an investment bank, released a survey of over 200 Hong Kong-based manufacturers operating in the Pearl River Delta. It found that wages have already risen by 10% this year. Foxconn, a Taiwanese contract manufacturer that makes Apple’s iPads (and much more besides) in Shenzhen, put up salaries by 16-25% last month.

“It’s not cheap like it used to be,” laments Dale Weathington of Kolcraft, an American firm that uses contract manufacturers to make prams in southern China. Labour costs have surged by 20% a year for the past four years, he grumbles. China’s coastal provinces are losing their power to suck workers out of the hinterland. These migrant workers often go home during the Chinese New Year break. In previous years 95% of Mr Weathington’s staff returned. This year only 85% did.

Kolcraft’s experience is typical. When the American Chamber of Commerce in Shanghai asked its members recently about their biggest challenges, 91% mentioned “rising costs”. Corruption and piracy were far behind. Labour costs (including benefits) for blue-collar workers in Guangdong rose by 12% a year, in dollar terms, from 2002 to 2009; in Shanghai, 14% a year. Roland Berger, a consultancy, reckons the comparable figure was only 8% in the Philippines and 1% in Mexico.

Joerg Wuttke, a veteran industrialist with the EU Chamber of Commerce in China, predicts that the cost to manufacture in China could soar twofold or even threefold by 2020. AlixPartners, a consultancy, offers this intriguing extrapolation: if China’s currency and shipping costs were to rise by 5% annually and wages were to go up by 30% a year, by 2015 it would be just as cheap to make things in North America as to make them in China and ship them there (see chart). In reality, the convergence will probably be slower. But the trend is clear.

If cheap China is fading, what will replace it? Will factories shift to poorer countries with cheaper labour? That is the conventional wisdom, but it is wrong.

Advantage China

Brian Noll of PPC, which makes connectors for televisions, says his firm seriously considered moving its operations to Vietnam. Labour was cheaper there, but Vietnam lacked reliable suppliers of services such as nickel plating, heat treatment and special stamping. In the end, PPC decided not to leave China. Instead, it is automating more processes in its factory near Shanghai, replacing some (but not all) workers with machines.

Labour costs are often 30% lower in countries other than China, says John Rice, GE’s vice chairman, but this is typically more than offset by other problems, especially the lack of a reliable supply chain. GE did open a new plant in Vietnam to make wind turbines, but Mr Rice insists that talent was the lure, not cheap labour. Thanks to a big government shipyard nearby, his plant was able to hire world-class welders. Except in commodity businesses, “competence will always trump cost,” he says.

Sunil Gidumal, a Hong Kong-based entrepreneur, makes tin boxes that Harrods, Marks & Spencer and other retailers use to hold biscuits. Wages, which make up a third of his costs, have doubled in the past four years at his factories in Guangdong. Workers in Sri Lanka are 35-40% cheaper, he says, but he finds them less efficient. So he is keeping a smaller factory in China to serve America and China’s domestic market. Only the tins bound for Europe are made in Sri Lanka, since shipping costs are lower than from China.

Louis Kuijs of the Fung Global Institute, a think-tank, observes that some low-tech, labour-intensive industries, such as T-shirts and cheap trainers, have already left China. And some firms are employing a “China + 1” strategy, opening just one factory in another country to test the waters and provide a back-up.

But coastal China has enduring strengths, despite soaring costs. First, it is close to the booming Chinese domestic market. This is a huge advantage. No other country has so many newly pecunious consumers clamouring for stuff.

Second, Chinese wages may be rising fast, but so is Chinese productivity. The precise numbers are disputed, but the trend is not. Chinese workers are paid more because they are producing more.

Third, China is huge. Its labour pool is large and flexible enough to accommodate seasonal industries that make Christmas lights or toys, says Ivo Naumann of AlixPartners. In response to sudden demand, a Chinese factory making iPhones was able to rouse 8,000 workers from their dormitory and put them on the assembly line at midnight, according to the New York Times. Not the next day. Midnight. Nowhere else are such feats feasible.

Fourth, China’s supply chain is sophisticated and supple. Professor Zheng Yusheng of the Cheung Kong Graduate School of Business argues that the right way to measure manufacturing competitiveness is not by comparing labour costs alone, but by comparing entire supply chains. Even if labour costs are a quarter of those in China to make a given product, the unreliability or unavailability of many components may make it uneconomic to make things elsewhere.

Dwight Nordstrom of Pacific Resources International, a manufacturing consultancy, reckons China’s supply chain for electronics manufacturers is so good that “there is no stopping the juggernaut” for at least ten to 20 years. This same advantage applies to low-tech industries, too. Paul Stocker of Topline, a shoe exporter with dozens of contract plants in coastal China, says there is no easy alternative to China.

It is fashionable to predict that China’s inland factories will supplant its coastal ones. Official figures for foreign direct investment support this view: some inland provinces, such as Chongqing, now attract almost as much foreign money as Shanghai. The reason why fewer migrant workers from the hinterland are returning to coastal factories this year is that there are plenty of jobs closer to home.

But manufacturers are not simply shifting inland in search of cheap labour. For one thing, it is not much cheaper. Huawei, a large Chinese telecoms firm, reports that salaries for engineers with a master’s degree are not even 10% lower in its inland locations than in Shenzhen. Kolcraft considered shifting to Hubei, but found that total costs would end up being only 5-10% lower than on the coast.

Topline looked into moving inland, but found huge extra costs there. Infrastructure for exports is still shoddy or slow (shipping by river adds a week), logistics are not fully developed and Topline’s entire supply chain remains on the coast. It decided to stay put.

Inland revenue?

Moving inland brings all sorts of unexpected costs. Newish labour laws in wealthy places such as Shenzhen make it costlier to shut down plants there, for example. It can cost more to ship goods from the Chinese interior to the coast than from Shanghai to New York. Managers and other highly skilled staff often demand steep pay rises to move from sophisticated coastal cities to the boondocks. Chongqing has more than 30m people, but it’s not Shanghai. A recent anti-corruption campaign there grew so violent that it terrified legitimate businessfolk as well as crooks.

The firms investing in China’s interior are chiefly doing so to serve consumers who live there. With so many inland cities booming, this is an enticing market. But when it comes to making iPads and smartphones for export, the world’s workshop will remain in China’s coastal provinces.

In time, of course, other places will build better roads and ports and supply chains. Eventually, they will challenge coastal China’s grip on basic manufacturing. So if China is to flourish, its manufacturers must move up the value chain. Rather than bolting together sophisticated products designed elsewhere, they need to do more design work themselves. Taking a leaf out of Germany’s book, they need to make products with higher margins and offer services to complement them.

A few Chinese firms have started to do this already. A visit to Huawei’s huge corporate campus in Shenzhen is instructive. The firm was founded by a former military officer and has been helped by friends in government over the years, but it now more closely resembles a Western high-tech firm than it does a state-backed behemoth. Its managers are top-flight. Its leaders have for several years been learning from dozens of resident advisers from IBM and other American consultancies. It has become highly professional, and impressively innovative.

In 2008 it filed for more international patents than any other firm. Earlier this year, it unveiled the world’s thinnest and fastest smartphones. In a sign that at least China’s private sector is beginning to take intellectual-property rights seriously, Huawei is locked in bitter battles over patents, not only with multinationals but also with ZTE, a cross-town rival that also wants to shift from being a low-cost telecoms-equipment maker to a creator of sexy new consumer products.

China does not yet have enough Huaweis. But it attracts plenty of bright young people who would like to build one. Every year another wave of “sea turtles”—Chinese who have studied or worked abroad—returns home. Many have mixed with the world’s best engineers at MIT and Stanford. Many have seen first-handhow Silicon Valley works. Indeed, Silicon Valley veterans have founded many of China’s most innovative firms, such as Baidu.

The pace of change in China has been so startling that it is hard to keep up. The old stereotypes about low-wage sweatshops are as out-of-date as Mao suits. The next phase will be interesting: China must innovate or slow down.

from the print edition | Business

筆者對原文的回應

Fears of a hard landing

Mar 17th 2012, 07:15

The Economist described the importance of China’s industry of manufacture last week, and this issue has writings talking about the vision of Chinese economy. Undeniably, it is China that plays the role of contemporary world economy’s generator. The cause-effect of finance with business in manufacture are closely related to the whole gross economy. For half a year, Beijing has adjusted inner financial policy and bureaucracy, well-prepared for the war of yuan-dollar. Last week, the start of next stage was shown in Two-Conference’s press conference, where China’s prime minister Wen Jia-bao made last address in National People’s Congress during his tenure.

After Mr. Wen announced the preview of GDP’s growth, the target of 7.5%, the most of analysts inclines negative attitude. Similar to the view of this article, the overall speed of Chinese growing economy seems to slow down to less than 8% for a while according to Financial Times’ Kate Mackenzie on Mar. 13. So did JPMorgan’s strategist Adrian Mowat, on Mar. 14 in Singapore. And some predicts reflecting on the car sales in recent forecasts cannot reach the expectation because the excitement of government hardly overtake the fuel prices. However, something goes smooth when it comes to Beijing striving for lessening inflation, including reducing loans and retail sales which make Beijing more room to ease monetary policy.

At this critical point, the future vision of Chinese economy mostly depends on manufacture, including rising wage, automobile line’s knowledge of supply-demand chain in the market, and the employee’s skill as well as the researcher’s potential; moreover, the attention to six-sigma of management is essentially keeping the momentum of enterprise helping expanding economy. Of course, the healthy surroundings for investors, mainly owing to the policy by People’s Bank of China (PBOC), could ensure the establishment of the long-term prosperity. This circle of Chinese economy, or market economy, inevitably faces the case which any developing economy already experiences. Meanwhile, Beijing’s claim of “socialist democracy” could bring the better environment for foreigner direct investment (FDI), decreasing some impedement in China in line with the upcoming fifth generation of China’s Communist Party (CCP). Based on macroeconomy, keeping the low loan, low consumer price index (CPI) adding to steady property prices will sustain Chinese economy if either facing the trade deficit or experiencing another period of economic growth.

China follows the path of Japan and some newly-industrializing economies (NIEs). A book “Business Growth Strategies for Asia-Pacific”, written by Acer’s Shih Zhen-rong (Stan Shih) and other two, referred to the brand of value on a basis of industrial Research and Development (R&D), including the evolving technology and shifting the manufacture to competence, with the accumulation of practical examples and case studies as time goes by. Like Japan and Taiwan, there are some examples which Chinese can learn from, from clothes industry’s Uniqlo of Tadashi Yanai, to heavy industrial Toyota’s Akio Toyoda and Co Fujio, Hon-Hai's Guo Tai-min (Terry Guo), HTC’s Wang Shei-hung (Cherr Wang), the above’s Acer’s Stan Shih, Samsung’s Lee Kun-Hee and Lee Jae-Yong (Jay Y. Lee). The mutual character contains the international cooperation with other fields, the well-organized development, better know-how in industrial banking, and the most - the gain in brand recognition in market.

Spending nearly one generation struggling for rich wealth in Asia, China is qualified to show the complacency with higher level of manufacture such as high-tech, also reflecting on the value of various kinds of brand name, from the early Haier, Lenovo and China Mobile to the rising E-commerce like Alibaba, Baidu. Furthermore, there are famously stories achieving several good grades in China’s business attributable to not only their individuals but also all the world, especially in the third world, such as Haier’s Zhang Rui-min, Lenovo’s Yang Yuan-qing, Sany’s Liang Wen-gen, Hun Dai’s Hsu Jia-ing, Wan Ke’s Wang Shi and Alibaba’s Ma Yun (Jack Ma). To respect these kinds is another way to assist in the generator world economy, different from the whole visionary predict.

To strengthen industrial competitiveness is the first that Chinese be aware of during China’s industrial structure change. With the change, the control of inflation as well as supervision of prices fluctuation may be taken into consideration for the long-standing development and guarantee of every year (constantly at least annual 7%) until the number of per capita GDP reaches the level of at least that of NIEs twenty years ago (I guess more than U.S.D.16000). China has the best cause of inducement to invest in BRICs. Even if the growth number is below 8%, relatively, China’s economy is more prosperous than other’s. It is not sensible at all if criticizing too much.

Recommended

10

Report

Permalink

筆者當年是一起回覆兩篇原文在討論區上。今天中美貿易逆差更大,導致貿易大戰又要開打了。中國商務部(2018年2月7日,中央社報導)公布數據,美國去年對外逆差貨品達8100億美元,其中,美中之間的逆差有3752億美元,占了46%以上。3月22日川普總統簽署備忘錄,希望一年內削減1000億美元的逆差,開啟了新一起的漣漪和導致中俄的更緊密關係。

這篇倒是作借題發揮,在歐巴馬對稀有金屬作制裁時,那天日美等國覺得逆差不夠大。筆者當時聊了一下中國廉價勞力的減少倒也是經濟轉型的契機,就提了一本施振榮和張忠謀寫給John Wiley的亞太企業成長策略,從序言列出各發展中國家較細經濟數據,而後分了十個部份舉十間亞洲企業和歐美成熟相關領域翹楚的比較。這裡的確偏重工業和資訊科技業的比較,也在各行業來說較顯著貢獻成長。筆者稍微舉例台灣、韓國的科技業大老,同時提到像萬科Vanke王石,和在2008年及去年重回中國首富的恒大Evergrande創辦人許家印,筆者有各一本這兩位的不動產天王的傳記:「我怎麼成為世界第一:王石的道路與夢想」(這是和繆川寫的自傳,台灣版是時周出版),「恒大傳奇:解密中國首富許家印」(人民日報出版社,2011,張守剛)。兩本都很勵志。筆者除了是在楊中美博士的書認識馬雲,就是和現任政協主席汪洋在廣東省委書記任上的電子化政府,也在2010年11月經濟學人雜誌business欄上詳讀其能力培養過程。

因此筆者當時認為中國政府若能維持有低物價通貨膨漲及低貸款率(即公債和資產比率的控制)得宜,就算遇到貿易逆差波動過劇,如今天的中美經濟情勢,中國的社會和經濟能有所緩衝,就算仍會有國內物價不穩定,政府已作夠延遲及心理準備。當然在這幾年間企業的成長和國際上的活動擴充了不少,比如研發能力足夠了些,也作像亞洲四小龍當年對中國大陸那般,在東南亞和非洲投資設廠,深圳如今(2018年)是中國最大軟體研發中心,在2012年這裡提及時,才嶄露頭角不到兩三年,仍然有一些是偏硬件代工性質的公司行號。隨著工資上漲,企業為了要獲利就是轉型,在珠三角一帶尤其明顯,聯想、華為及中興帶動的本地一條龍產業鏈,本國自主研發兼國內拼裝的能力,那時正在這附近起飛; 同時電子商務及行動金融的新生活型態也開始在一線,甚至二線城市普及,器物帶動思想及法制的維新這五六年間推動了新一代的年青人的創意飛舞,雖然有點扯遠,也許帶動中共的政治上變動是說不定的。

中國政府有良好的國際間國與國互動,以一帶一路及基礎建設經驗輸出為一個明顯的途徑,而今天中國經濟是一大挹注,循序漸近參與規則的制定和慣例的維持,而不是變成一種破壞它國主權的手段和威脅,同時要注意市場機制(中國製產品很有誘惑力)和國與國貿易平衡的問題,稍稍些緩了中國經濟的成長速率,這就是說中國努力作自己,希望突破世界經濟的每個經濟體的強弱關係、宿命論來解啦~

附上一篇之後更正圖片的說明:

Clanger: China's economy

Mar 24th 2012 | from the print edition

An error in London meant that our piece on China's economy last week ("Fears of a hard landing") was accompanied by a picture of a plane operated by China Airlines, a Taiwanese carrier.

Clanger: China's economy

Mar 26th 2012, 16:05

Oh, ha, that’s seemingly to say OK if you want to say Taiwan is one part of China.

In 1980-2000, Taipei’s China Airplane, which made so many historical records of air crash in the world, was so famous that you, the Economist, might pay attention to the common sense. Eek, there is somewhat unfortunate. Of course, China has no such airplane company running; moreover, hard-landing may be hard to happen in the near two decades. China's rising number of per capita GDP could be chasing the decreasing index in time.

Be careful of the source in the future.

Recommended

2

Report

Permalink

*附一篇4月21日報導以current-account追蹤中國經濟動態

China’s current-account surplus

Fair play or foul?

The Chinese yuan now looks close to its fair value

Apr 21st 2012 | from the print edition

· Tweet

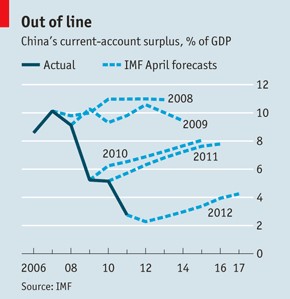

AT ITS peak, of over 10% of GDP in 2007, China’s current-account surplus offered firm proof that the yuan was undervalued. The evidence is much less conclusive now. China’s currency is 30% stronger in real trade-weighted terms than in 2005, when its peg to the dollar was scrapped. Partly as a result, the country’s current-account surplus fell to 2.8% of GDP last year.

Even the International Monetary Fund (IMF), which has been consistently more pessimistic than most economists (see chart), has slashed its forecasts for the surplus. The fund now expects it to dip to only 2.3% of GDP this year, and then to rise gradually to just above 4% of GDP by 2017 (compared with predictions in April 2011 of 6.3% and 8%, respectively). It may still be overegging things, even so. The IMF assumes that China’s real trade-weighted exchange rate will remain constant over the period. Because China has higher inflation than America, this oddly implies a steady depreciation in the yuan’s nominal rate against the dollar of 10% over the next five years. The forecast surplus would be smaller if you instead assume that the yuan’s nominal exchange rate will stay constant.

In this section

· »Fair play or foul?

The most common method for judging a currency’s fair value is to estimate the exchange rate needed to bring a country’s current-account imbalance to a “normal” level. The Peterson Institute for International Economics, a think-tank which has done lots of work in this area, reckons that a surplus or deficit of less than 3% of GDP is acceptable. The IMF’s new forecasts imply that China’s surplus will average 3.2% over the seven years to 2017. If this is so, it is hard to argue that the yuan is significantly undervalued.

Chinese officials have already said that the yuan is now close to its fair value. So far this year it has been broadly flat against the dollar. But that does not rule out further appreciation. First, although its overall trade surplus fell last year, China’s surplus with America rose to a record $202 billion, more than accounting for its total surplus (China ran a deficit with the rest of the world). To defuse mounting trade tensions, the Beijing government will remain under pressure to let the yuan climb against the dollar. Second, even if the yuan’s value is “correct” today, faster productivity growth than elsewhere means that China should continue to allow its real exchange rate to rise.

Most economists expect the yuan to resume its rise soon, but at a much slower pace than before and with greater flexibility up and down. On April 16th the People’s Bank of China (PBOC) doubled the size of the yuan’s daily trading band against the dollar to plus and minus 1% from a fixed midpoint. The immediate impact may be small: the yuan rarely hit its previous limits anyhow, and the PBOC will still set the midpoint each day. But it is a modest, welcome step towards allowing market forces to play a bigger role.

from the print edition | Finance and economics

*附同年二月兩篇經濟學人報導馬雲和阿里巴巴的文章

Alibaba.com

So long, for now

Feb 22nd 2012, 22:55 by V.V.V. | HONG KONG

One big motivation for delisting, the parent company said, is to have the freedom to run its offshoot “free from the pressure of market expectations, earnings visibility and share price fluctuations.” It also admitted that its slumping share price had been causing problems inside the company: “A depressed share price may continue to adversely impact?employee morale,” it said.

The deal, which will set Alibaba back $2.3 billion, looks likely to succeed. One reason to think so is the hefty premium on offer. A bit over a quarter of Alibaba.com’s shares are publicly traded, and the firm is offering those unhappy shareholders HK$13.50 ($1.74) per share. That matches the offer price of the firm’s initial public offering in 2007, and is roughly 46% higher than the last closing price two weeks ago, when trading in the firm’s shares were halted.

Another reason for shareholders to cash in may be that the division’s immediate commercial prospects look dim. The web portal is still recovering from a corruption scandal and has endured a backlash among users who are unhappy with recent changes to the way the site works. Jinkyu Yoon of Nomura, a stockbroker, adds that Alibaba.com’s core business model—charging small and medium-sized Chinese sellers a fee to be connected with buyers at home and abroad—is also under attack from big search engines like Google and a Chinese equivalent, Baidu.

Mr Ma argues that the delisting will give the group the space it needs to work out a new strategy for Alibaba.com, which will require investments that may reduce short-term returns. His managers have been shifting the division’s focus from expanding the number of paying vendors to curating a site with better quality and service. Such an approach, if it works, may be the best defence against commoditisation and the erosion of margins by competitors like the big search engines.

Still, there may also be other motives behind this week’s move. Yahoo! and Alibaba have tried to agree terms that would allow the Chinese firm to acquire the big stake in its parent group held by the American search firm, but those talks recently fell apart. Some investors wonder if the delisting will somehow make it easier for Mr Ma to buy back that stake. Others speculate that it is a first step towards a flotation of the whole Alibaba group.

The firm this week splashed cold water on both rumours. This “privatisation,” as delisting is called in Hong Kong, is strictly about sorting out Alibaba.com’s strategy, it insisted. Perhaps so, but punters keen to bet on China’s internet future will surely be watching Mr Ma’s moves closely.

· 4

Alibaba.com

So long, for now

Why the Chinese web portal is giving up its stockmarket listing

Feb 25th 2012 | HONG KONG | from the print edition

SHAREHOLDERS can be such nuisances. This week the Alibaba group, China’s biggest internet firm, announced that it wants to delist the shares of Alibaba.com, its business-to-business arm, that are traded on the Hong Kong stock exchange. The company, and its founder and chairman, Jack Ma, made no attempt to sugar-coat the decision.

One big motivation for delisting, the parent company said, is to have the freedom to run its offshoot “free from the pressure of market expectations, earnings visibility and share price fluctuations.” It also acknowledged that its slumping share price had been causing problems inside the company: “A depressed share price may continue to adversely impact…employee morale,” it said.

In this section

· »So long, for now

The deal, which will set Alibaba back $2.3 billion, looks likely to succeed. One reason to think so is the hefty premium on offer. A bit over a quarter of Alibaba.com’s shares are publicly traded, and the firm is buying out those unhappy investors for HK$13.50 ($1.74) per share. That matches the offer price of the firm’s initial public offering in 2007, and is roughly 46% higher than the last closing price two weeks ago, when trading in the firm’s shares was halted (see chart).

Another reason for shareholders to cash in may be that the division’s immediate prospects look dim. The web portal is still recovering from a corruption scandal and has endured a backlash among users who are unhappy with recent changes to the way the site works. Jinkyu Yoon of Nomura, a stockbroker, adds that the core business model of Alibaba.com—charging small and medium-sized Chinese sellers a fee to be connected with buyers at home and abroad—is also under attack from big search engines like Google and a Chinese equivalent, Baidu.

Mr Ma argues that the delisting will give the group the space it needs to work out a new strategy for Alibaba.com, which will require investments that may reduce short-term returns. His managers have been changing the division’s main objective from expanding the number of paying vendors to improving quality and service. Such an approach, if it works, may be the best defence against commoditisation and the erosion of margins by competitors like the big search engines.

Still, there may also be other motives behind this week’s move. Yahoo! and Alibaba have tried to agree terms that would allow the Chinese firm to acquire the big stake in its parent group held by the American search firm, but those talks recently fell apart. Some investors wonder if the delisting will somehow make it easier for Mr Ma to buy back that stake. Others speculate that it is a first step towards a flotation of the whole Alibaba group.

The firm this week splashed cold water on both rumours. This “privatisation”, as delisting is called in Hong Kong, is strictly about sorting out Alibaba.com’s strategy, it insisted. Perhaps so, but punters keen to bet on China’s internet future will surely be watching Mr Ma’s moves closely.

from the print edition | Business

下一則: Stoking the furnace Mar 8th 2012, 07:59

限會員,要發表迴響,請先登入